Investment thesis

Major contract underpins earnings prospects

On 2nd October 2017, Carimin secured a contract from PETRONAS Carigali for the provision of maintenance, construction and modification (MCM) services (Package C Offshore Peninsular Malaysia Oil) for a period of five years with an option to extend for one year. Other local contractors that won an MCM service package includes Dayang, Deleum, Petra Energy and Sapura Fabrication (JV with Borneo Seaoffshore Engineering, a subsidiary of Handal Resources). For clarification, PETRONAS Carigali awarded separate MCM packages to all these contractors and it is not an umbrella contract where every job needs to go through a mini-tender process.

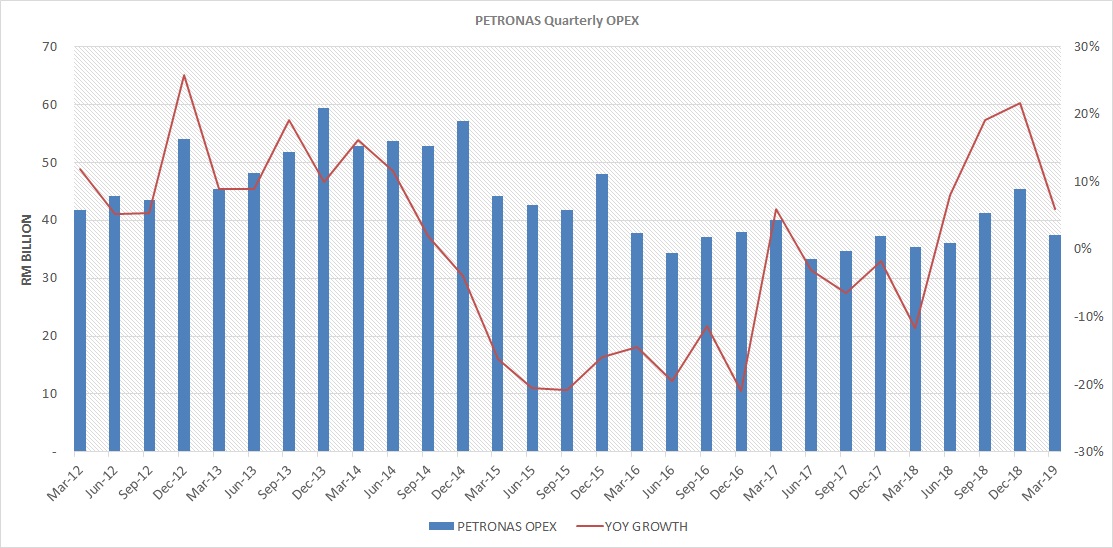

The MCM contract value was not specified in the announcement, but estimates suggest each package could be worth up to RM1b, which translates to roughly RM200m revenue per year. Barring a collapse in crude oil prices, we opine that activity levels under the package will be high in the near term as PETRONAS has been deferring or doing minimal maintenance works since 2015. This is imperitive in order to ensure the sustainability of upstream production. PETRONAS has been cutting back on opex since the end of 2014 and it has taken nearly four years for quarterly opex to exhibit y-o-y growth. Simply put, we are at the beginning of an opex upcycle.

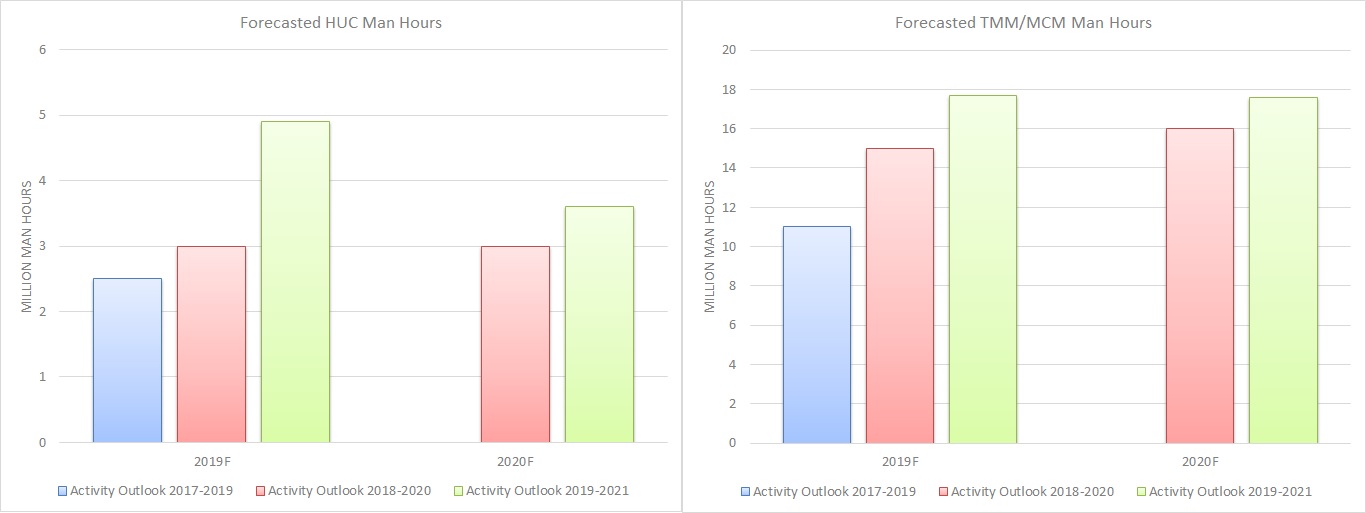

PETRONAS in its last three annual Activity Outlook reports have increasingly become more bullish for both HUC and TMM activities for 2019F and 2020F. It appears from the most recent (and likely most accurate) Activity Outlook, PETRONAS expects TMM/MCM man hours to remain constant at above 17m whilst HUC man hours will peak in 2019 with 4.9m man hours before normalising to 3.6m man hours.

A recovery in the works

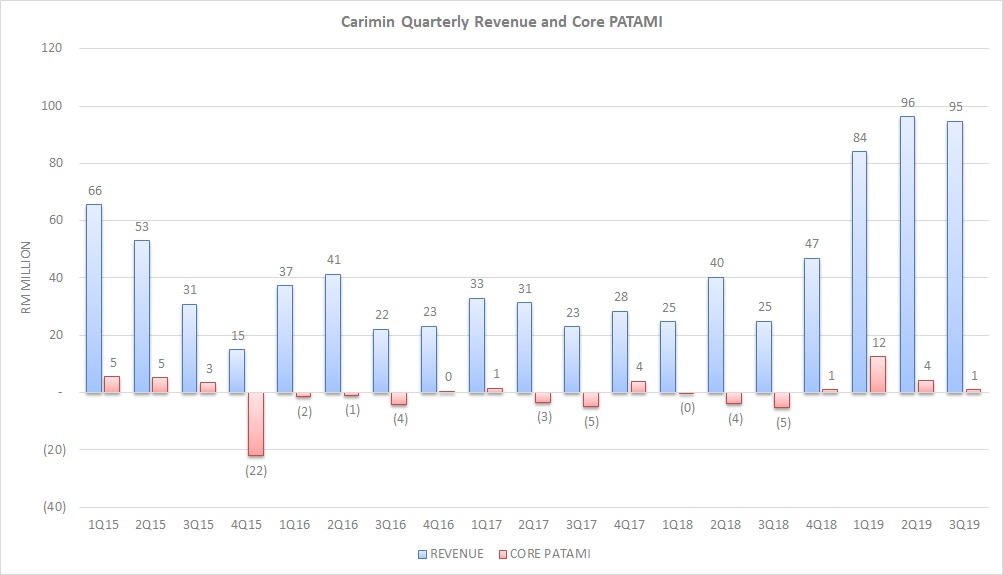

Beginning 1Q19 up til the most recent quarter, Carimin started to exhibit extremely strong y-o-y revenue growth. Revenue was up 340%, 239% and 381% y-o-y in 1Q19, 2Q19 and 3Q19, respectively. This was driven primarily by the HUC segment as well as its supporting maritime services business. In addition, core earnings have remained positive in the last four quarters after posting volatile results previously, with one impressive quarter, 1Q19, which delivered core earnings of RM12m.

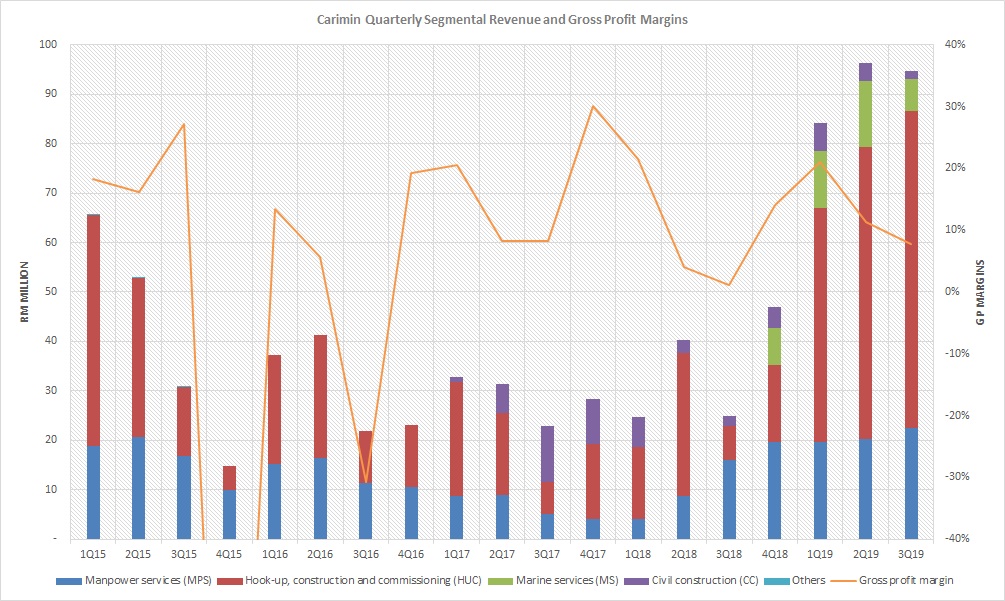

Carimin’s gross profit margins are seasonally driven. It peaks in 4Q (April to June) and 1Q (July to September) with the non-monsoon period and recedes in 2Q (October to December) and 3Q (January to March) with the monsoon period. During the monsoon period, the work done is largely onshore, which involves fabrication and preparation for offshore HUC or TMM. Margins are softer during this period because fabrication work is generally on a cost-plus basis and the company’s vessels are not working but manpower, depreciation and maintenance costs are still on-going. During the non-monsoon period, the client will perform scheduled shutdowns which then allows Carimin the opportunity to perform its HUC or TMM works. Offshore works will require a range of services including personnel, installation, workover services, maintenance, repairs and replacement parts and marine vessels. Overall, because of multiple services provided and utilisation of vessels, Carimin’s margins are higher.

Non-monsoon season means peak revenue, margins and earnings

Carimin: “Despite volatility in global oil price, there has been an increase in project activities and work orders. Major maintenance and hook up & commissioning works, rejuvenation, modification, field improvement projects, major blasting and painting including marine service works is expected increase as part of client’s integrity facilities management.”

Dayang: “Taking cue from the work orders in hand, we are hopeful that business operations will remain busy over the coming months which should augur well for our financial results… After securing the lion share of the Pan MCM contracts estimated at RM1.5-2b from multiple production sharing contractors in Malaysia in 2018, we are looking forward to going full steam ahead in 2019 to deliver all the work orders entrusted by our esteemed clients.”

However, the remaining MCM contractors such as Deleum and Petra Energy remain conservative regarding prospects, limiting their enthusiasm to being cautiously optimistic (in Petra’s case) or simply stating intentions to improve financial performance via various initiatives (in Deleum’s case). Overall though, taking cue from Carimin and Dayang’s statements it appears that circumstances and sentiment have turned for the better compared to previous years.

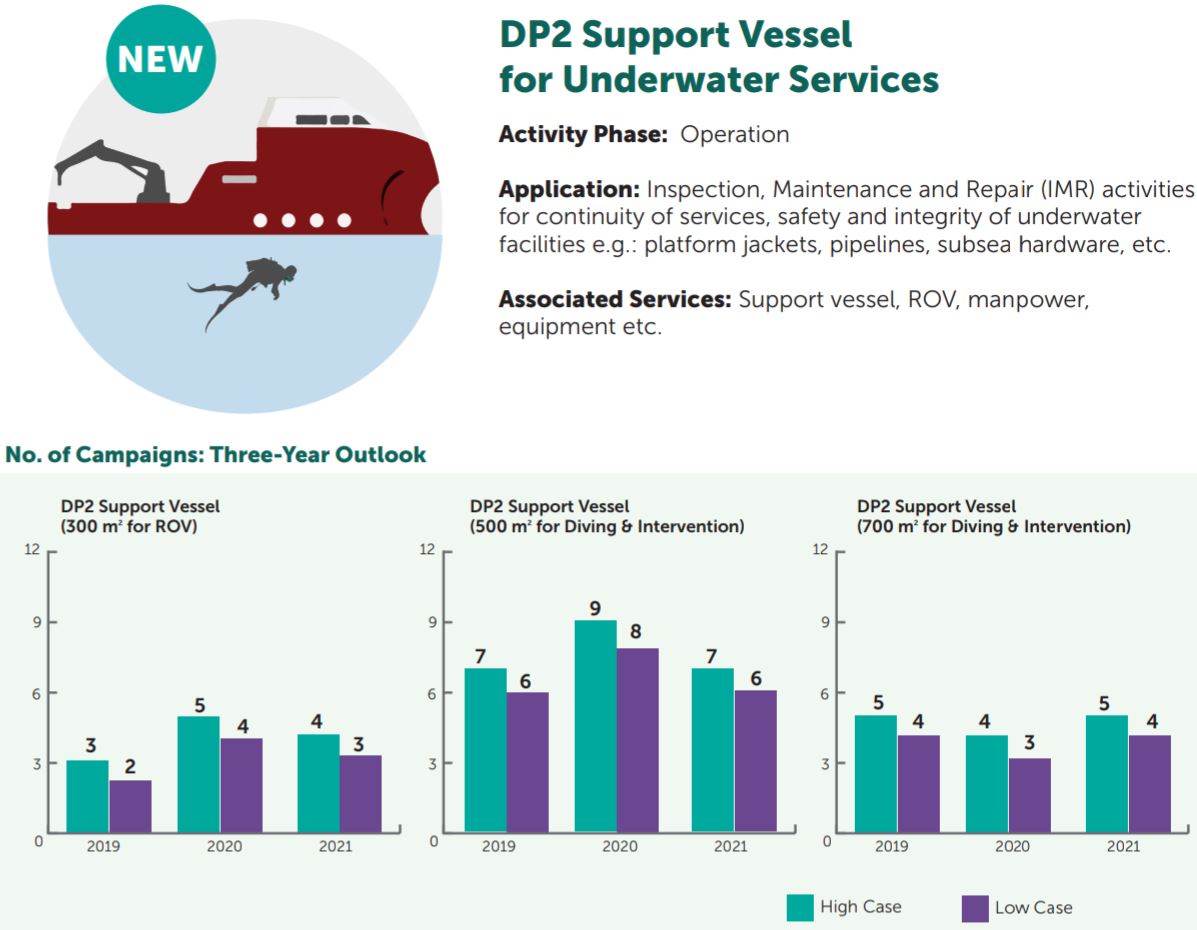

Diving into sub-sea with purchase of Subnautica

On 27th of March 2019, Carimin acquired a 60% interest in Subnautica Sdn Bhd for a cash consideration of RM35,659. Subnautica is licensed by PETRONAS to undertake sub-sea and underwater inspection, repair and maintenance works and services. Subnautica was awarded a contract for the provision of diving support vessel DP2 with inspection class ROV with competent personnel.

We view the move into sub-sea and underwater works positively as these services generally attract higher margins due to higher operational risks and is a natural extension to Carimin’s existing MCM business. According to PETRONAS’ 2019-2021 Activity Outlook it expects 2-3 campaigns in 2019, followed by 4-5 campaigns in 2020 and 3-4 campaigns in 2021 in the DP2 support vessel (300m for ROV) category. PETRONAS introduced a new groupwide Frame Agreement with a panel of vendors in 2018 which will expire in 2023 of which Subnautica is part of.

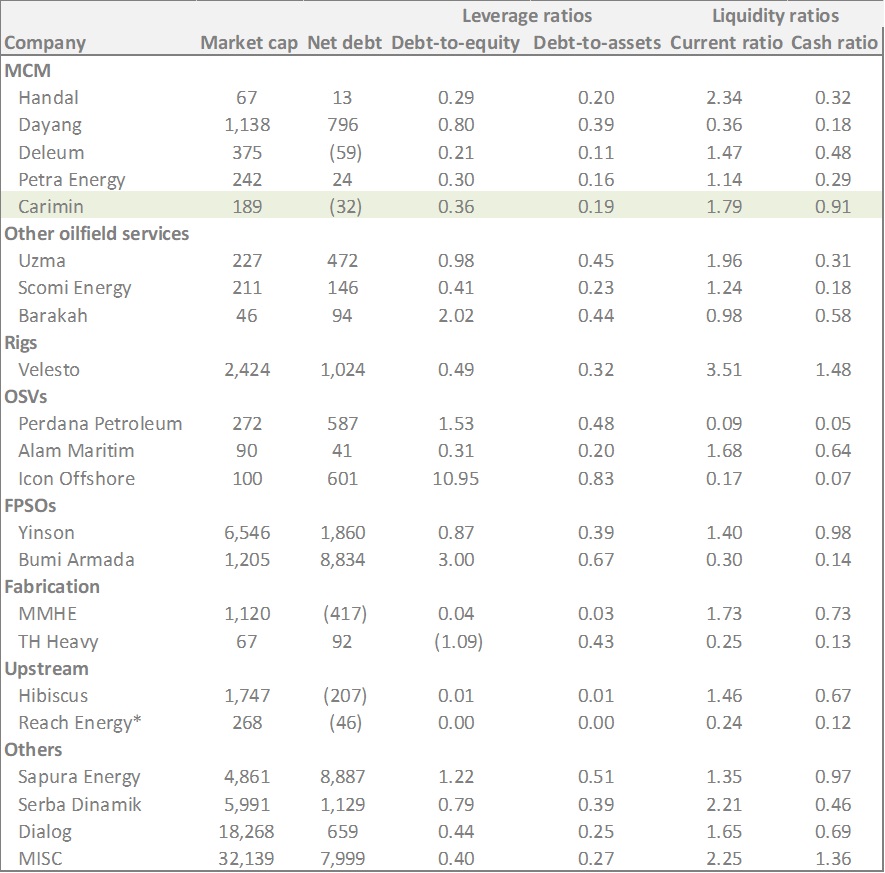

One of the healthier balance sheets for an oil & gas company

Relative to the majority of domestic oil & gas companies, Carimin’s balance sheet appears healthy. As at 31st March 2019, Carimin had a debt-to-equity ratio of 0.36x. It is in a net cash position of RM32m with healthy current and cash ratios of 1.79x and 0.91x, respectively.

* Reach Energy’s debt is understated as it has shareholder loans which has not been classified as debt

Started paying dividends again

After four quarters of being profitable, on the 23rd May 2019, Carimin announced a first interim dividend of 1.4 sen per share for FY2019 amounting to RM3.2m. The dividend is to be paid 28 June 2019. This is the first dividend payout since 2015.

To be continued…

PART 3: Forecasts, valuation and risks

To receive the full unredacted research report please subscribe to our mailing list. Link is on the sidebar.