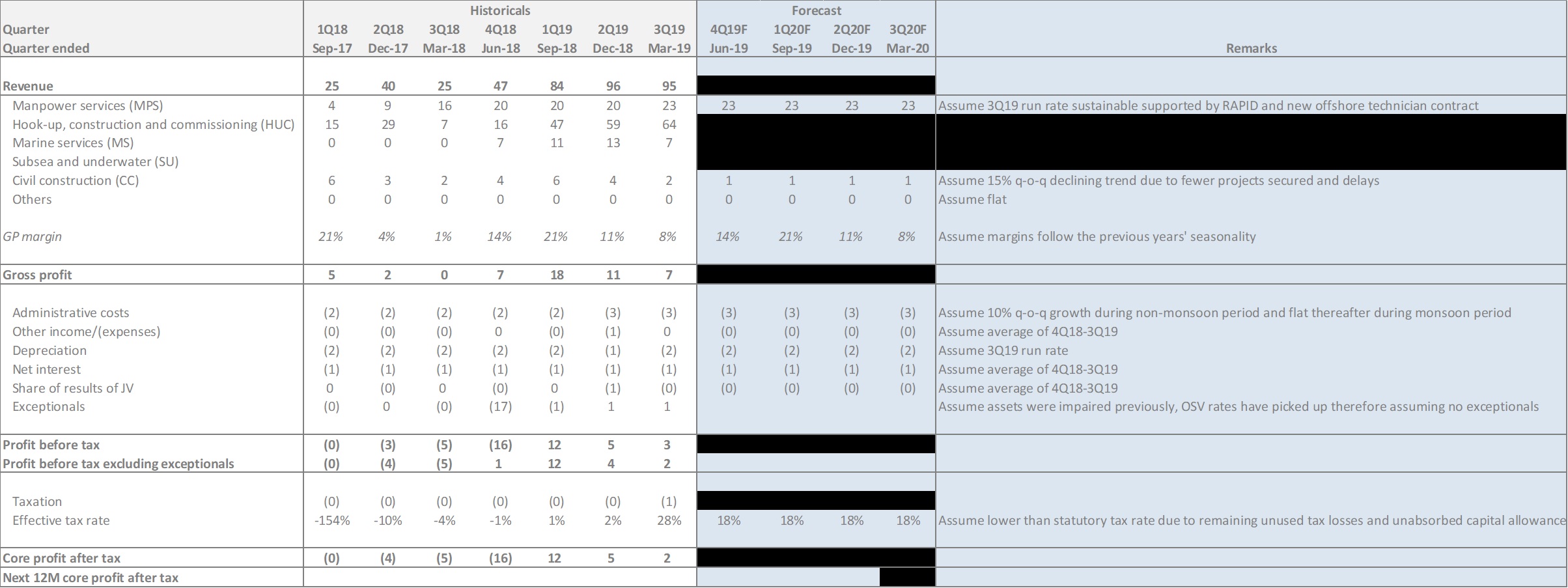

Forecasts

Admittedly, it is difficult to forecast Carimin’s financials accurately as it depends on the work schedule permitted by PETRONAS, additional work orders, weather, unplanned delays, etc which is not readily available. However, we can formulate guestimates by deriving the relative growth between PETRONAS’ forecast TMM/MCM and HUC man hours between 2018 and 2019.

For HUC segment, PETRONAS in Activity Outlook 2018-2020 forecasted 4.0m man hours in 2018 and in the most recent Activity Outlook forecasted 4.9m man hours in 2019. Assuming these are the most accurate forecasts because of the shorter time frame, we derive HUC activity y-o-y growth to be 22.5%. Applying a similar methodology to TMM segment, we derive that y-o-y activity growth should approximate 18% based on PETRONAS’ forecast of 15.0m man hours in 2018 and 17.7m man hours in 2019.

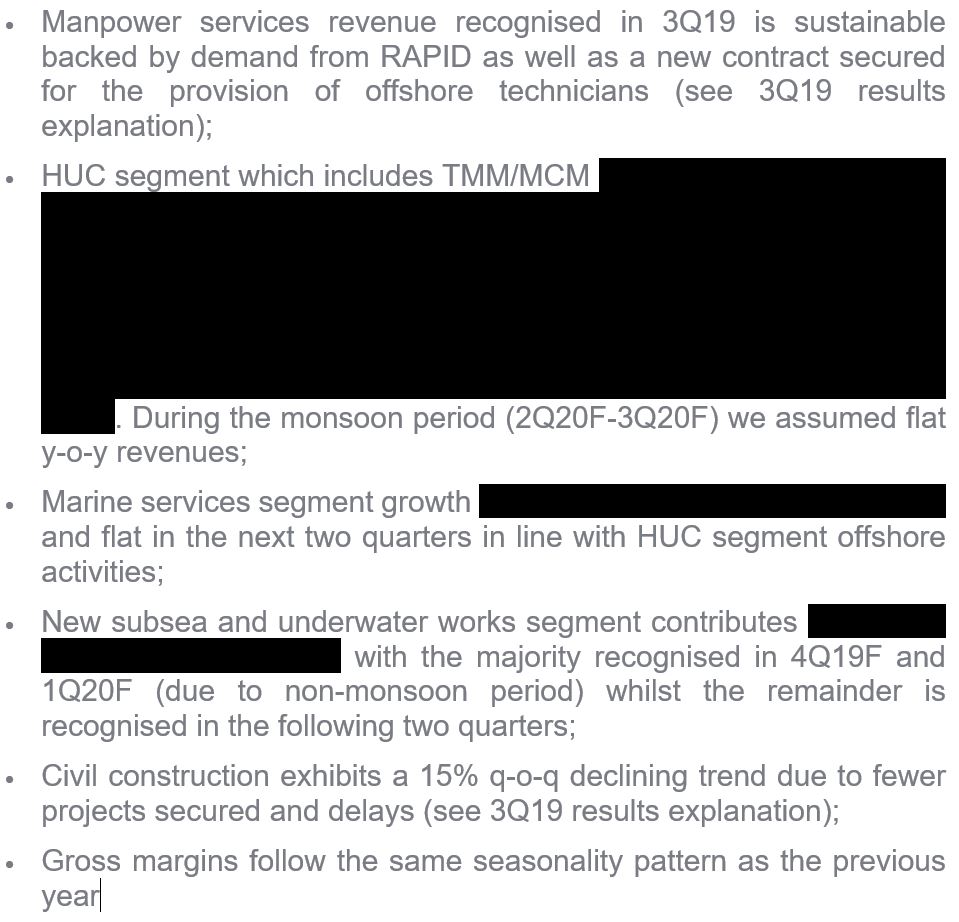

Based on this encouraging macro environment, we have conservatively assumed:

To reiterate, we have used conservative assumptions in order to derive forecasts which we think builds in a large margin of safety. We could (and probably should) have assumed higher growth rates for HUC and Marine Services segment based on the level of activity and number of vessels in operation suggested by our channel checks highlighted in Part 2 of this report.

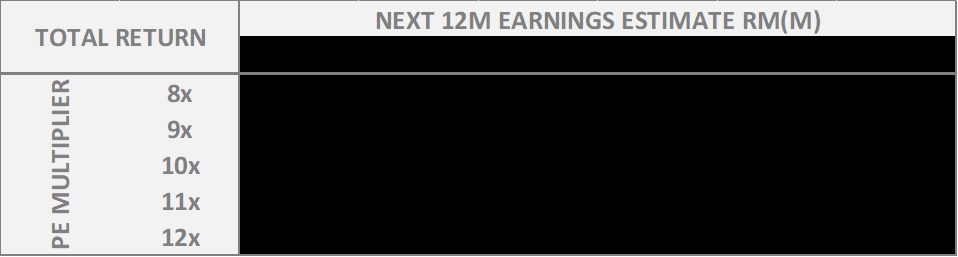

Valuation

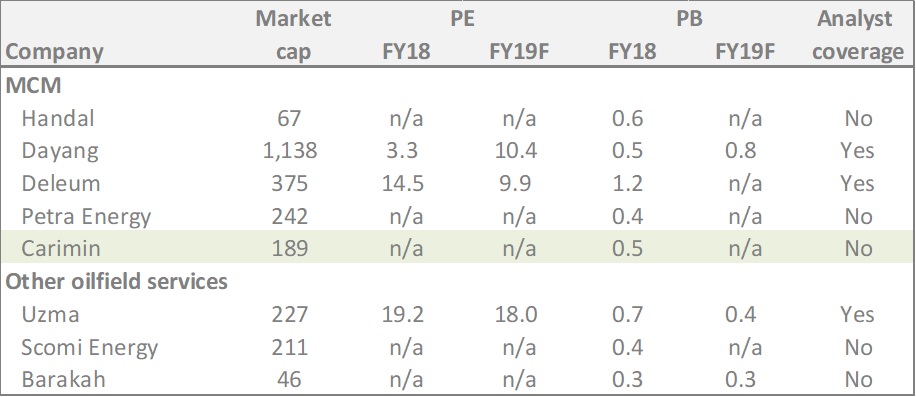

We used the other winners of PETRONAS’ MCM packages as well as other companies involved in oilfield services as peers to Carimin. However, out of the seven identified peers, only three are covered by analysts with forward projections. Clearly, Dayang and Deleum are the closest peers and both are trading at approximately 10x forward PE.

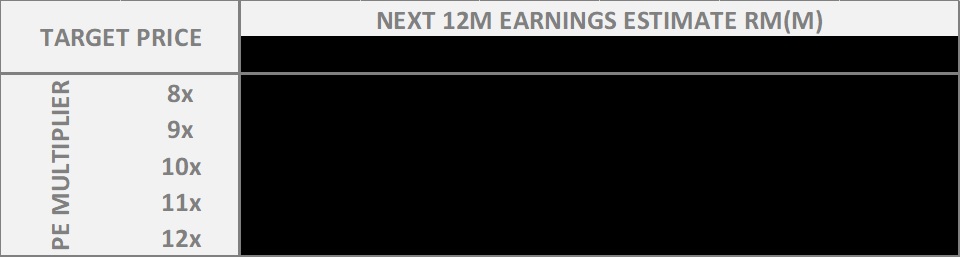

As mentioned earlier, we believe our next 12M earnings estimate to be conservative. Hence, we have included a range of potential valuations if earnings come in stronger-than-expected. Also, note that valuations in the Oil & Gas sector rely very much on sentiment which is driven by crude oil prices. If crude oil prices fall or rise significantly, the PE multipliers may also vary.

Risks

Sharp decline in oil prices

Despite our confidence in PETRONAS having to proceed with maintenance works in order to ensure sustainability of production, any fall in crude oil prices will surely dampen sentiment around the oil & gas sector. Given that the last downturn is still fresh on people’s minds, we expect any sharp decline in crude oil prices to result in a sell down in the oil & gas sector and Carimin is no exception.

Given the volatility in crude oil prices in the past year we think it is very difficult to give any assurance that oil prices will remain in this USD60-70/bbl range. However, it is important to keep in mind that there are risks on both the demand and supply side. Demand may falter if global growth slows and with the protracted trade war this risk is becoming significant. On the supply-side, US oil exports are growing but this is mitigated by OPEC supply side cuts, tensions in the Middle East and disruptions in Venezuela and Iran.

Execution risk

Efficient project execution is essential for Carimin to recognize the revenue and attractive margins on a certain project. Delays and hiccups in execution results in cost overruns and slower revenue recognition. The client may also penalise Carimin by retracting the contract and awarding it to another party if execution is sub-optimal.

While it is difficult to predict the outcome in terms of execution of projects especially in an offshore environment which is affected by weather and other external forces, we can be comforted by the fact that Carimin’s track record in the HUC space has not been blemished by any negative events to our knowledge. Furthermore, maintenance is the least risky activity in the oil & gas supply chain.