Business description

Carimin is primarily a domestic oil & gas service provider specialising in: 1) Construction, Hook Up, Commissioning (HUC) and Top Side Major Maintenance (TMM), 2) Manpower Services (MPS) and 3) Marine Services (MS). Following the prolonged downturn in crude oil prices, Carimin also diversified into civil construction (CC) in 2017.

Financial history

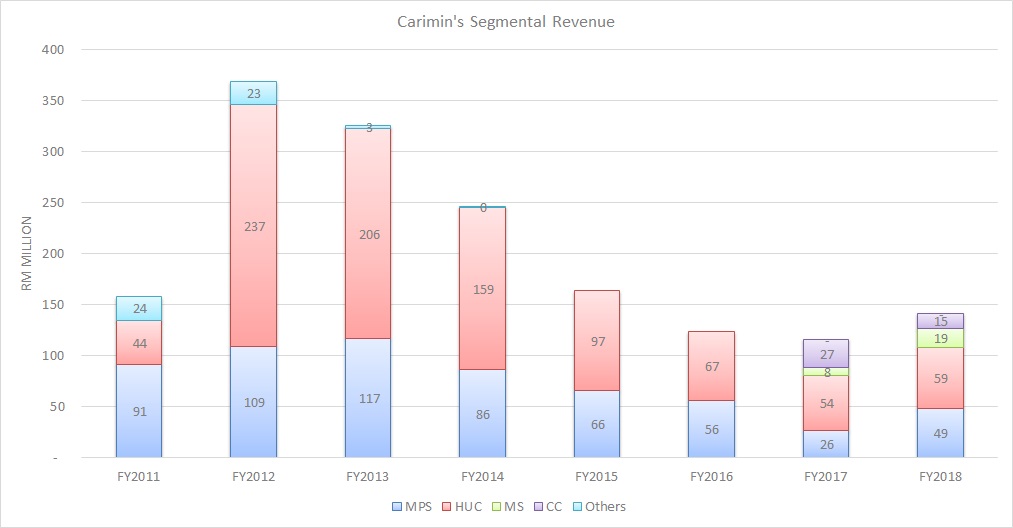

In FY2011, Carimin derived 57% of its revenue from MPS followed by 28% in HUC and 15% from other sources. The following financial year, Carimin’s HUC business became its main focus with the segment reporting revenue growth of 4.4x y-o-y from RM44m to RM237m. As a result, HUC made up 64% of total revenue underpinned by substantial work billings from the provision of offshore hook up and commissioning for PETRONAS Carigali facilities for a two-year period (Sarawak / Sabah HUC Contract). In FY2013, Carimin recorded lower revenue from HUC segment as work orders began to taper in line with PETRONAS Carigali’s new term master programme for the Peninsular HUC Contract.

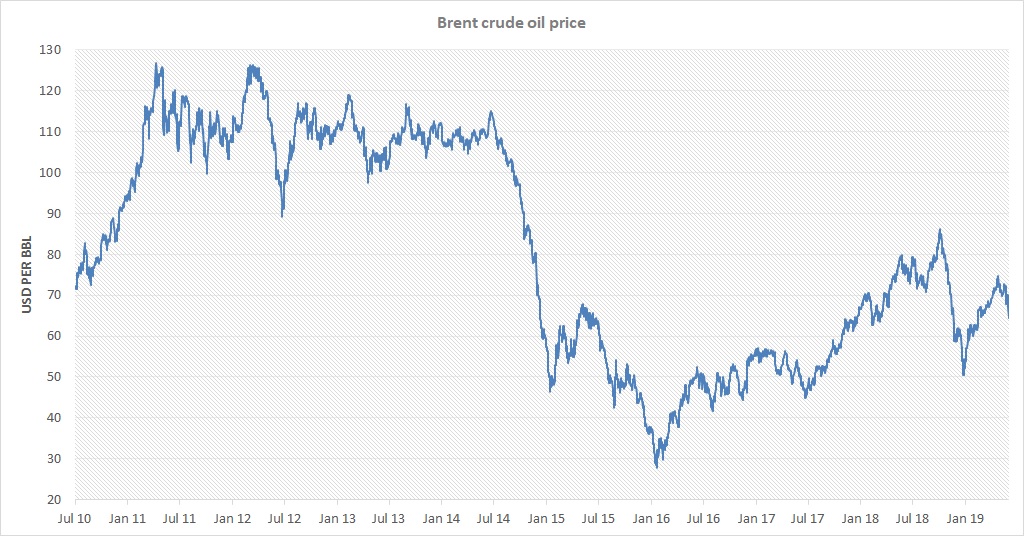

Mid-2014, crude oil prices began a sharp descent from above USD100/bbl to below USD60/bbl by year-end. This descent continued until 2016 and resulted in a prolonged downturn in the Malaysian oil & gas sector. Carimin went public in November 2014, just after the start of the downturn and has had to endure a difficult beginning as a publicly-listed entity.

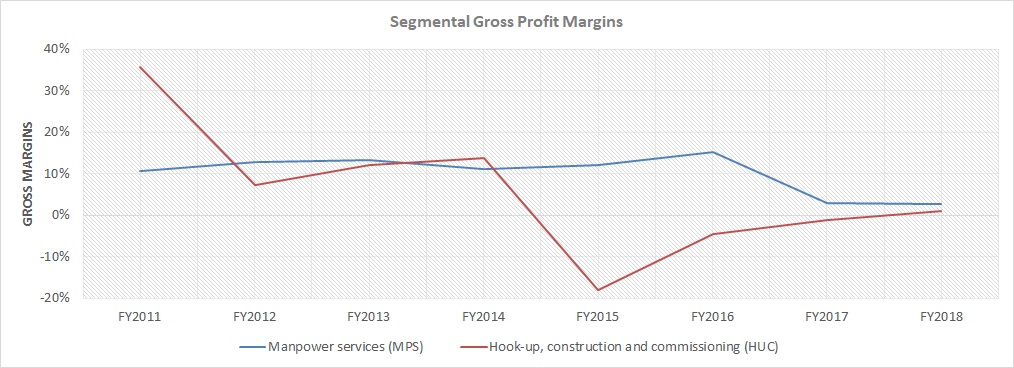

During the heydays of FY2011-FY2014, gross profit margins for the MPS segment was approximately 11-13% due to the scarcity of qualified personnel. However, following the downturn, margins for this segment have shrunk to circa 3% due to a combination of lower demand and PETRONAS recognising the low value add of this type of service.

For the HUC and TTM segment, gross profit margins have been volatile and this is down to the project oriented nature of the business which is dependent on winning contracts and efficiency of execution which is subject to client requirements, schedules and weather. Margins are also affected by the type of work performed ie. technical requirements, risk and utilisation of assets.

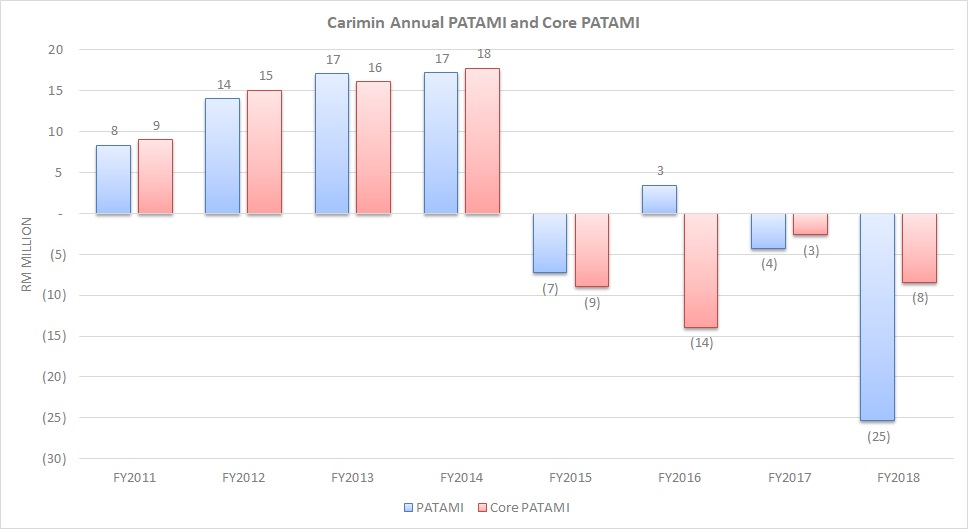

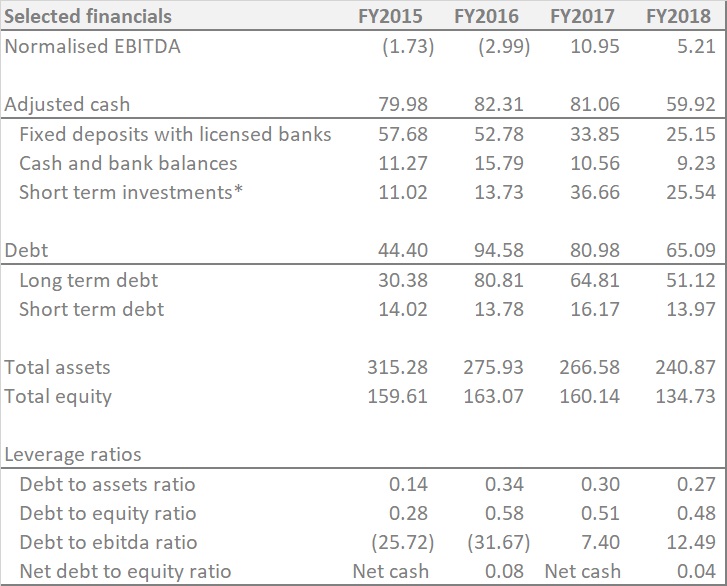

From FY2015 onwards due to weak crude oil prices, PETRONAS embarked on cost-cutting measures for both OPEX and CAPEX which resulted in projects being deferred or cancelled and ultimately caused a slowdown in activities and significant downward pressure on rates. Despite the downturn, Carimin remained resilient and was able to pull through without accumulating substantial losses. The company recorded headline RM8m loss in FY2015, RM3m profit in FY2016, RM4m loss in FY2017 and RM25m loss in FY2018. After excluding exceptional items such as forex gains/(losses), impairments to PPE and trade receivables as well as recognition of fair value gains, core LATAMI was RM9m, RM14m, RM3m and RM8m in the last four financial years, respectively. Management was able to consolidate resources, renegotiate supply agreements, introduce cost-cutting measures as well as enhance efficiencies during this difficult period.

Carimin’s balance sheet also remained resilient unlike most oil & gas companies during the downturn. As recently as FY2017, the company was in a net cash position. As at FY2018-end the company’s net debt to equity ratio was a mere 0.04x. The company also did not do any equity fund-raising in the last four years. This indicates that management has been careful and prudent in managing its debt levels.

*Adjusted cash includes short term investments which are investments in money market funds

To be continued…

Part 2: Investment thesis

To receive the full unredacted research report please subscribe to our mailing list. Link is on the sidebar.