4Q19 core earnings 30% ahead of our forecasts

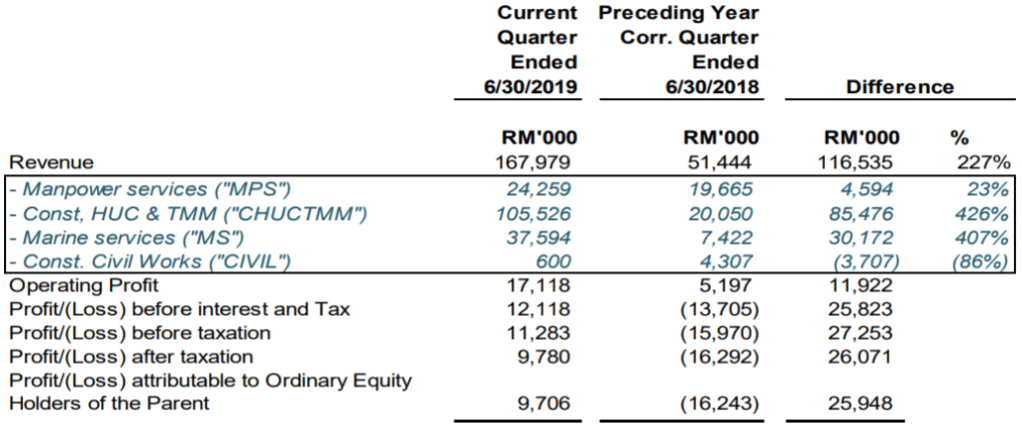

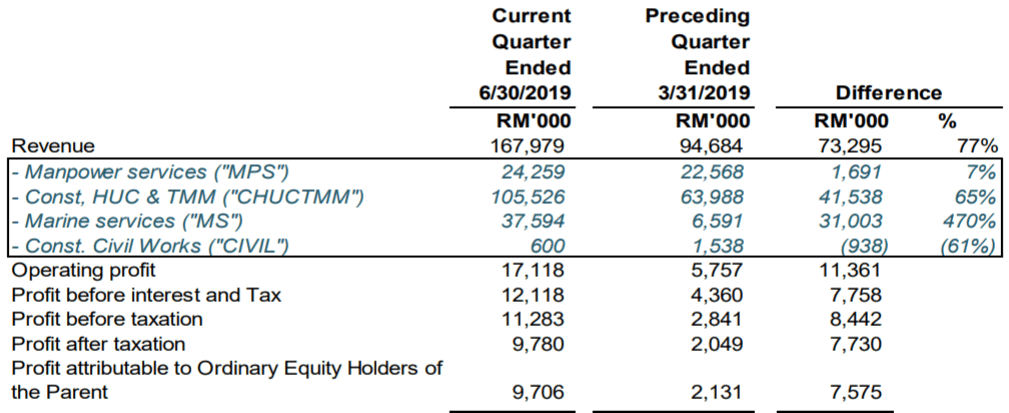

Carimin recorded headline earnings of RM9.7m which reversed a loss of RM15.9m in the same period last year. On a qoq basis, headline earnings were up nearly 356% from a RM2.1m base. But to get a better understanding of the numbers, lets strip out the one-offs and non-cash exceptional items.

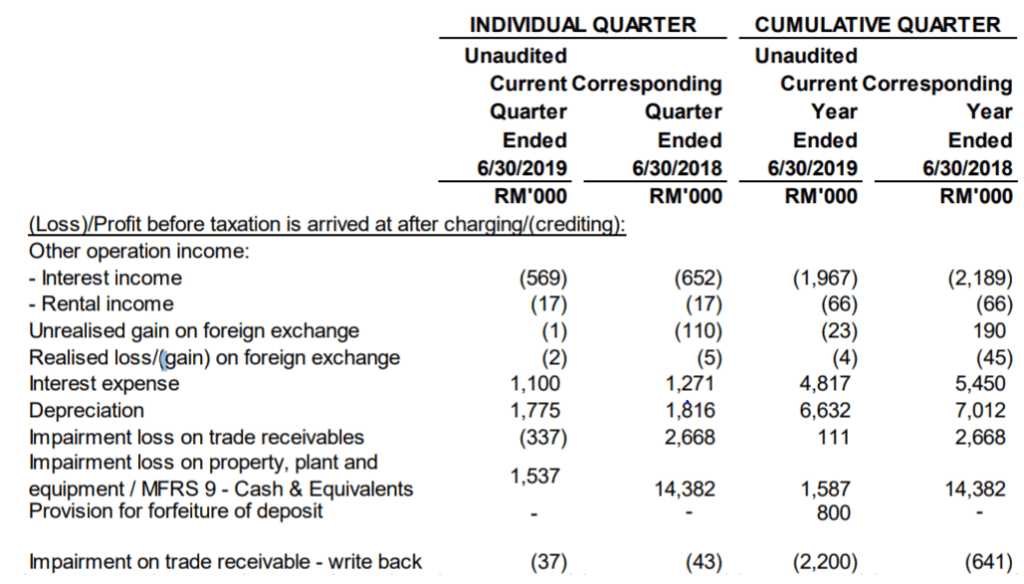

After stripping out the following non-core items: 1) unrealised gain on forex, 2) realised gain on forex, 3) writebacks on impairment loss on trade receivables, and 4) impairment loss on property, plant and equipment, Carimin’s core earnings come in at RM10.9m.

Recall in our research report “Cari-cari minyak, minyak sudah jumpa”, we estimated that Carimin would do approximately RM8.4m this quarter. Therefore, headline and core earnings were actually 16% and 30% ahead of our estimates, respectively.

Understanding what went right and what went wrong

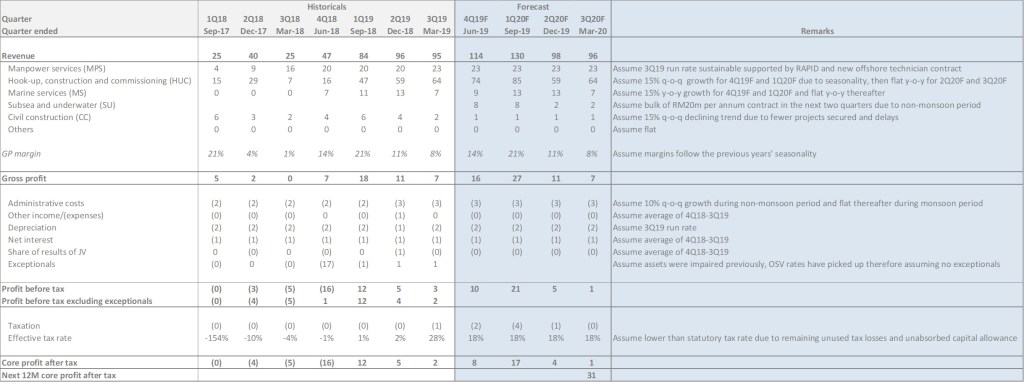

Revenues came in much stronger than expected, up 258% yoy and 77% qoq and was ahead of our forecasts by 47%. This was mainly due to the strong showing of the Construction, HUC and TMM (CHUCTMM) and Marine Services (MS) divisions.

CHUCTMM and MS division showed strong growth due to increased offshore activies and higher utilisation rate for its marine vessels which included a diving support vessel (DSV) for underwater service. Offshore activities increased because of a major shut down whilst the high demand for vessels drove the MS division.

Despite the strong topline growth, margins were not as attractive as initially estimated. We targeted a gross profit margin of 14% versus the actual gross profit margin of 11%. The quarterly report did not indicate why this was so, however, we guess it may be due to initial cost outlays for chartering vessels, hiring of new labour and other preparatory costs for offshore activities. We will be trying to get more insight from our channel checks.

Something to look forward to

Going forward, we are still very positive for 1Q20, when offshore activities are at its peak and Carimin historically derives its fattest gross profit margins. We understand that for 4Q19 most of the revenue for CHUCTMM was derived from one major shut down. For 1Q20 we expect Carimin to be working on two major shut downs – one was initially supposed to start in June but was postponed to July, whereas another should start towards the end of the quarter.

Recall also that on the 18th of July 2019, Carimin was awarded a two year contract for the provision of mechanical and piping maintenance services for Labuan Crude Oil Terminal. We understand that Carimin has already received its first workorder with a value of approximately RM15m.

Another surprise dividend

Together with the 4Q19 results, Carimin announced a second interim dividend of 1.6 sen per share bringing total dividends to 3 sen this year. This equates to a dividend yield of 3.125% based on yesterdays closing of 96 sen.

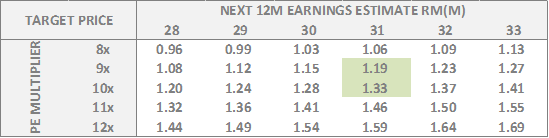

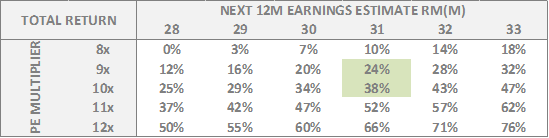

Still plenty of upside

We maintain our forecasts for now pending more clarification on level of activity and gross profit margins in 1Q20 despite actual headline and core earnings being ahead of our forecasts by a significant amount (>10%). On a trailing 12 months basis, Carimin trades at 7.8x PE, is a RM25m NET CASH company with a decent dividend yield of 3.125%. We continue to advocate a BUY and maintain our RM1.26 target